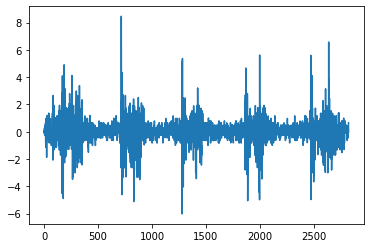

I have a time series with periodicities like that shown in the attached image. I am trying to build a forecasting model which I can sample trajectories.

For the most part the approach like in the pyro tutorials of using covariates with a weight gives something that looks vaguely like what I want:

The main problem is that I cannot capture the periodic short impulses that occur I’m guessing because I have a Gaussian prior for my weights. I think this failure is also making the noise too strong in regions where it shouldn’t be (in between peaks).

I have also tried using StudentT, Cauchy and Stable distributions for my weights but this produces worse results. I’m guessing I need another term to capture these short pulses.

Any ideas how this can be done? The model has to be generative.