Hi,

I am using numpyro version 0.12.1 on Mac.

I intend to use DiscreteHMCGibbs on a simple non-Markovian regime switching time series model.

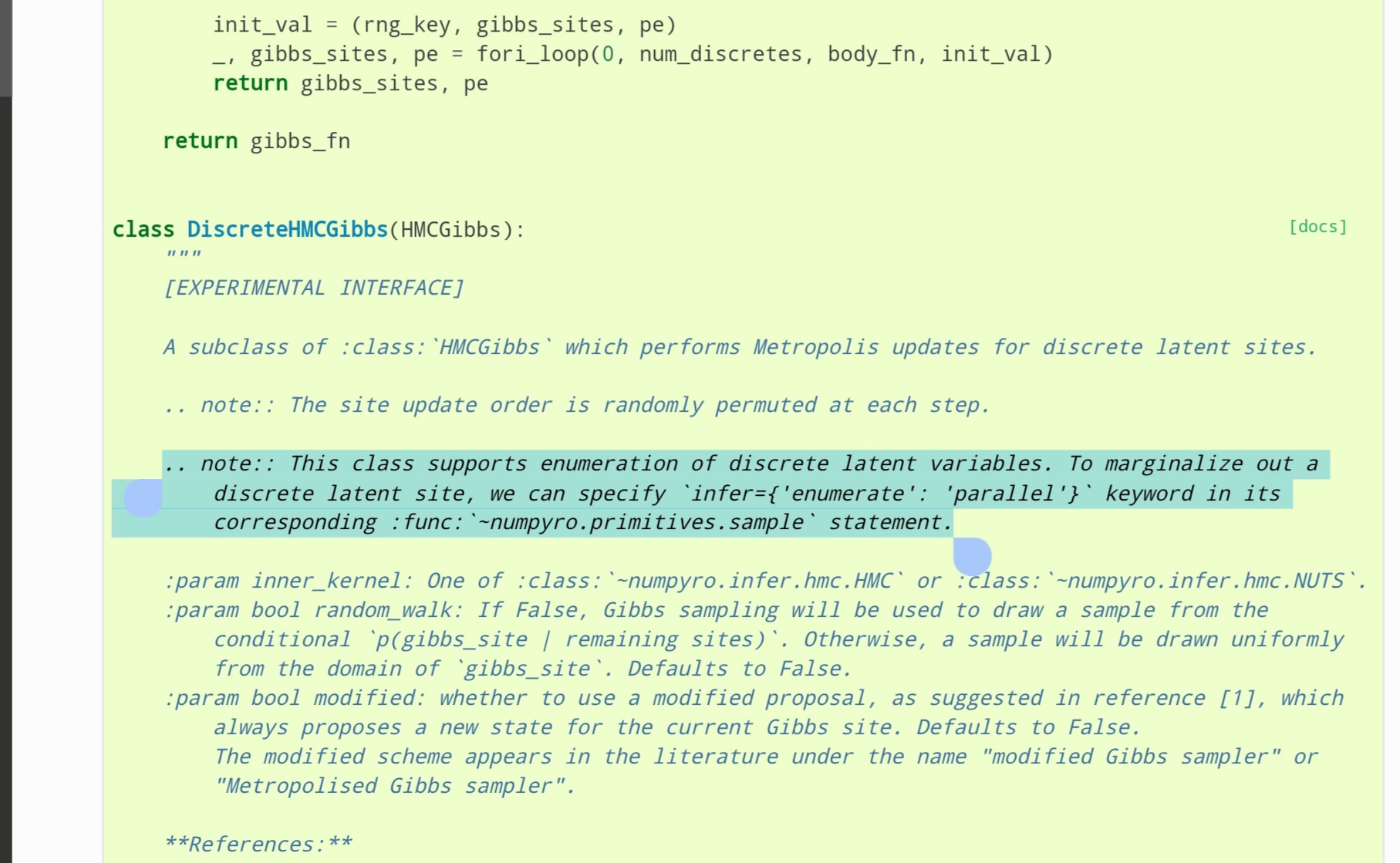

I saw on the doc that the module can marginalize out a discrete latent in the model by setting the infer enumerate to parallel.

While I think the model contains discrete latent variables, the DiscreteHMCGibbs says it does not.

The (unrealistic) simplified version of the model I am working on is shown below:

def RS_AR1(y):

theta = numpyro.sample("theta", dist.Normal().expand([2]).to_event(1))

def transition_func(carry, y):

prev_y = carry

next_regime_prob = jax.nn.sigmoid(prev_y)

current_regime = numpyro.sample("current_regime", dist.Bernoulli(next_regime_prob),

infer={'enumerate': 'parallel'})

current_theta = theta[current_regime]

current_y = numpyro.sample("current_y", dist.Normal(current_theta * prev_y), obs = y)

return (current_y), None

carry_init = (y[0])

scan(transition_func, carry_init, y[1:])

ar1_kernel = DiscreteHMCGibbs(HMC(RS_AR1))

mcmc_1 = MCMC(ar1_kernel, num_samples = 10000,num_warmup = 10000)

mcmc_1.run(random.PRNGKey(1), jnp.array(y))

Basically, the parameter for the time series model vary between two values determined by probability determined by the sigmoid of the output in the previous time step.

I got “AssertionError: Cannot detect any discrete latent variables in the model.”

How can I fix this? Or Any suggestion on this.

Note: 1. I removed the “infer=…”. the code runs, but it does not marginalize out “current_regime.”

2. got the same problem for NUTS innner kernel. Also the same problem for MixedHMC.

3. I also tried on “Markov Switching” (with parallel enumerate), and it works well.

Thank you for any helps